Retirement planning is often put off until “later,” but the truth is, the sooner you start saving for retirement, the better. Delaying retirement savings significantly impacts your future financial security. This article will explore the compelling reasons why you should begin building your retirement nest egg today, highlighting the power of compounding and the long-term benefits of early planning. We’ll delve into practical strategies to make saving easier, regardless of your current financial situation, empowering you to secure a comfortable and worry-free retirement.

Ignoring retirement planning can lead to serious consequences. The longer you wait, the more money you’ll need to save each month to achieve your retirement goals. This is due to the crucial concept of compound interest, where your earnings generate further earnings over time. Starting early allows you to harness the power of compounding, maximizing your returns and significantly increasing your retirement savings. This article will provide you with the knowledge and motivation needed to start your retirement savings journey now, paving the way for a more secure and fulfilling future.

Time Is Your Greatest Asset

When it comes to securing a comfortable retirement, time is arguably your most valuable asset. This isn’t simply a matter of having more years to save; it’s about leveraging the power of compound interest.

Compound interest is the interest you earn on your initial investment, plus the accumulated interest from previous periods. The longer your money has to grow, the more significant the impact of compounding becomes. Starting early allows your investments to benefit from this exponential growth over a much longer timeframe.

Consider this: even small, consistent contributions made early in your career will accumulate substantially more over several decades than larger contributions made later in life. This is due to the extended period of compound growth. The earlier you start, the less you need to contribute each month to reach your retirement goals.

Furthermore, starting early allows for greater flexibility. If you begin saving early and experience market fluctuations, you have more time to recover potential losses. Later starts leave you with less time to make up for any setbacks.

In short, the benefits of early saving are undeniable. The longer you wait, the harder you will have to work to achieve the same retirement outcome. Time is not only money; it’s the catalyst for building wealth and securing a financially secure future.

How Compound Interest Builds Wealth

Compound interest is the eighth wonder of the world, as Albert Einstein is often quoted as saying. It’s the snowball effect of earning interest on your initial investment, principal, and also on the accumulated interest itself. This means your money earns money, exponentially growing your wealth over time.

Let’s illustrate with a simple example. Suppose you invest $10,000 with a 7% annual interest rate. In the first year, you earn $700 in interest. However, in the second year, you earn interest not only on the initial $10,000 but also on that accumulated $700, resulting in a higher interest earning. This compounding effect accelerates your investment growth significantly.

The longer your money remains invested, the more dramatic the impact of compounding becomes. The time value of money is a critical concept here; the earlier you start saving, the more time your investments have to grow exponentially. This extended timeline allows your initial investment to balloon into a considerably larger sum, maximizing the power of compounding.

Furthermore, the interest rate plays a crucial role. Even a small increase in the interest rate can significantly impact the final amount. While you may not always be able to control the interest rate, choosing higher-yield investment options can improve your returns over the long run.

In essence, understanding and harnessing the power of compound interest is paramount for building lasting wealth. By starting early and consistently contributing to your savings, you can leverage this powerful tool to secure a comfortable retirement.

Start With What You Can Afford

One of the biggest hurdles to starting a retirement savings plan is the perception that it requires a significant financial commitment. This couldn’t be further from the truth. The most important aspect is to begin, regardless of the amount. Even small, consistent contributions can yield significant returns over time thanks to the power of compound interest.

Many retirement plans, including 401(k)s and IRAs, have no minimum contribution requirements. This means you can start with as little as $10 or $25 per paycheck. While this might seem insignificant initially, it establishes a crucial habit of regular saving. As your income increases, you can progressively increase your contribution amount.

Consistency is more valuable than the initial contribution size. It’s better to save a small amount consistently than to make sporadic large contributions. The regular act of saving will instill a disciplined approach to your finances, which will be beneficial in other areas of your life as well.

Don’t let the fear of not having enough money prevent you from starting. Begin with what you can realistically afford, even if it’s a small amount. Over time, you can adjust your contributions as your financial situation improves. This incremental approach will make saving for retirement feel less daunting and more manageable. The key is to start now and build from there.

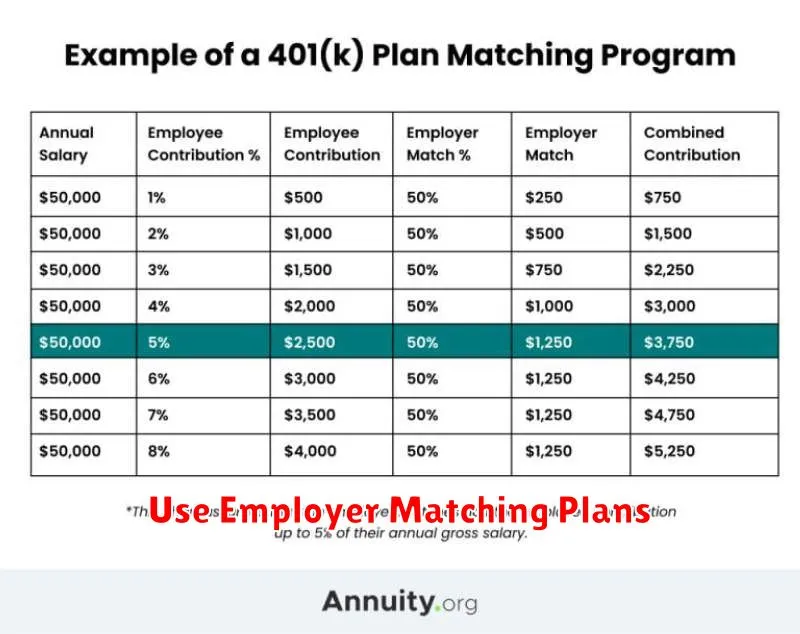

Use Employer Matching Plans

One of the easiest ways to boost your retirement savings is to take full advantage of your employer’s matching contributions. Many companies offer a plan where they’ll match a percentage of the money you contribute to your 401(k) or similar retirement plan, often up to a certain limit. This is essentially free money; it’s money your employer is giving you to invest in your future.

Don’t leave free money on the table. If your employer offers a matching contribution, contribute at least enough to receive the full match. This significantly increases your retirement savings without requiring any additional out-of-pocket expense from you. Consider it a guaranteed return on your investment, making it one of the smartest financial moves you can make.

Understanding your employer’s matching plan is crucial. Carefully review the details of the program, including the matching percentage, the contribution limits, and any vesting schedules (how long you must work for the company to fully own the employer’s matching contributions). This information is usually available in your employee handbook or through your human resources department.

Actively participating in your employer’s matching plan demonstrates proactive financial planning. It showcases responsibility and sets the stage for a more secure financial future. By maximizing employer matching, you lay a solid foundation for a comfortable retirement, effectively leveraging your current resources for long-term gains.

Review and Adjust Annually

Regular review of your retirement savings plan is crucial for ensuring you stay on track to meet your financial goals. Life circumstances change, and your savings strategy should adapt accordingly.

Annual review allows you to assess your progress and make necessary adjustments. This includes evaluating your current savings rate, investment performance, and any changes to your anticipated retirement needs. For instance, a change in job, salary, or family size may require reevaluating your contribution amounts or investment allocation.

During your annual assessment, consider factors such as inflation, changes in tax laws, and potential shifts in your risk tolerance. You may find it beneficial to adjust your investment portfolio to align with your revised timeline and risk appetite. Perhaps you need to increase your contributions to compensate for any shortfall or rebalance your portfolio to minimize risk as you approach retirement.

Professional guidance can be invaluable during this process. A financial advisor can help you analyze your progress, identify potential areas for improvement, and create a customized strategy to help you achieve your retirement objectives. They can also help you navigate complex financial decisions and adapt your plan to unforeseen circumstances.

In short, consistent annual review and adjustment of your retirement savings plan is not merely recommended; it’s essential for maximizing your retirement savings and securing a comfortable financial future.

Don’t Wait for a Perfect Moment

The most common reason people delay starting their retirement savings is the belief that they need to wait for the “perfect moment.” This is a dangerous fallacy. There is no such thing as a perfect time to begin investing for retirement; life is full of unforeseen circumstances and unexpected events.

Waiting for a higher income, a lower debt load, or a more stable job only pushes the start date further into the future. The power of compounding is significantly reduced the longer you wait. Each year you delay is a year of potential growth you miss, and catching up becomes exponentially harder over time.

Even small, regular contributions add up dramatically over the long term. Starting early, even with a small amount, allows your investments to grow and benefit from the effects of compounding interest. You may be surprised at how quickly your savings accumulate when given enough time to flourish.

Instead of waiting for an elusive perfect moment, focus on starting now, even if it’s with a small contribution. You can always increase your contributions as your income and circumstances allow. The key is to establish a consistent saving habit and take advantage of the time available for your money to grow.

Remember, consistency and time are your greatest allies in building a secure retirement. Don’t let the pursuit of perfection paralyze you into inaction. Start saving today.

{kind=link}