Creating a simple budget can seem daunting, but it’s a crucial step towards achieving your financial goals. This guide outlines best practices for building a manageable and effective budget that works for you, regardless of your income level. We’ll cover everything from tracking your spending and identifying areas for savings to setting realistic financial goals and avoiding common budgeting mistakes. Learn how to gain control of your finances and pave the way for a more secure financial future.

Mastering the art of budgeting doesn’t require complex spreadsheets or financial software. This article simplifies the process, providing clear, actionable steps to create a simple budget that’s easy to understand and maintain. Discover practical strategies for managing your money effectively, including tips on reducing expenses, increasing income, and building an emergency fund. With a well-structured budget, you can confidently navigate unexpected expenses, plan for major purchases, and ultimately, work towards financial freedom.

Start With Your Net Income

The foundation of any successful budget is understanding your net income. This is the amount of money you actually receive after taxes and other deductions are taken out of your gross income. Focusing on your net income, rather than your gross income, provides a more accurate reflection of the funds available for budgeting.

To determine your net income, refer to your pay stubs or your tax documents. These documents clearly outline your earnings and the deductions applied. It’s crucial to be precise in this calculation; using an inaccurate figure will lead to an ineffective budget.

Once you have determined your net income, you have a concrete number to work with. This figure represents the total amount available to allocate across your various expenses and savings goals. Understanding this number is the first crucial step in responsible financial planning.

Consider tracking your net income for several months to establish a reliable average. This is particularly useful if your income fluctuates due to bonuses, overtime pay, or irregular employment.

Categorize Spending With Priorities First

Creating a simple yet effective budget begins with categorizing your spending. This isn’t just about listing every expense; it’s about prioritizing needs versus wants and understanding where your money actually goes.

Start by identifying your essential expenses. These are the non-negotiables: housing (rent or mortgage), utilities (electricity, water, gas), food, transportation, and debt payments (minimum payments on loans and credit cards). These should form the foundation of your budget.

Next, categorize your non-essential spending. This is where you’ll see the areas for potential savings. Examples include entertainment (movies, dining out), clothing, subscriptions (streaming services, gym memberships), and personal care. Be as specific as possible; breaking down categories further will give you a clearer picture of your spending habits.

Once categorized, you can then prioritize. While all essential expenses are important, consider if there’s any room for optimization within those categories. For instance, can you find cheaper grocery options or reduce your energy consumption? For non-essential spending, identify areas where you’re overspending and can realistically cut back.

Using a spreadsheet or budgeting app can greatly simplify this process. Many apps allow for automated categorization, making tracking your spending much easier. The key is to be consistent in recording your expenses, so you can accurately assess your spending patterns over time and make informed decisions.

Choose a System That Works (50/30/20, Zero-Based, etc.)

Creating a simple budget starts with selecting a budgeting system that aligns with your personality and financial goals. There’s no one-size-fits-all solution, so exploring different methods is crucial. Popular options include the 50/30/20 rule, the zero-based budget, and various envelope budgeting systems.

The 50/30/20 rule is a straightforward approach. It suggests allocating 50% of your after-tax income to needs (housing, food, transportation), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. Its simplicity makes it an excellent starting point for beginners.

Alternatively, a zero-based budget requires more meticulous planning. This method involves allocating every dollar of your income to a specific category, ensuring that your income minus your expenses equals zero. While demanding initially, it offers a comprehensive overview of your finances and promotes mindful spending.

Envelope budgeting, a physical cash-based system, involves assigning specific cash amounts to different categories (groceries, gas, entertainment) and placing them in separate envelopes. Once an envelope is empty, spending in that category stops until the next budgeting cycle. This tactile approach can be very effective for visual learners and those who need to curb impulsive spending.

Ultimately, the best system is the one you can consistently maintain. Experiment with different methods to discover which one best suits your spending habits and financial objectives. Consider your level of comfort with detailed tracking and your overall financial goals when making your choice. Regularly reviewing and adjusting your chosen system is also essential.

Track Every Dollar Spent Weekly

Tracking your spending is fundamental to effective budgeting. While monthly overviews are helpful, a weekly review provides a more granular perspective, allowing for quicker identification and correction of spending patterns.

The key is consistency. Dedicate a specific time each week – perhaps Sunday evening or Monday morning – to review your transactions. Use whatever method works best for you: a spreadsheet, budgeting app, or even a simple notebook. The important thing is to capture every expense, no matter how small.

Categorizing your spending is also crucial. Common categories include housing, transportation, food, entertainment, and debt payments. By categorizing, you can easily identify areas where you’re overspending and pinpoint opportunities for saving.

This weekly tracking allows for immediate feedback. If you notice you’re consistently exceeding your budget in a particular area, you can make adjustments that week, preventing larger overspending problems down the line. It’s a proactive approach to financial management, enabling you to maintain control and stay on track with your financial goals.

Remember, the goal is not to restrict spending unnecessarily, but to gain a clear understanding of your financial habits. This awareness will be invaluable in making informed decisions and building a sustainable budget.

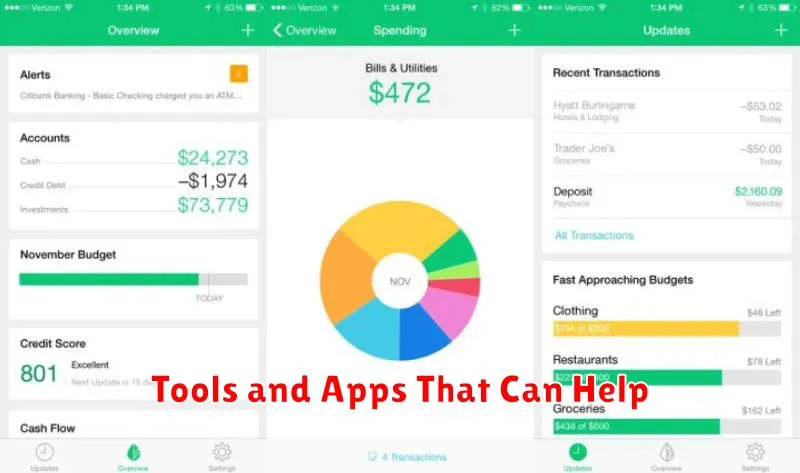

Tools and Apps That Can Help

Creating and maintaining a budget doesn’t have to be a daunting task. Numerous tools and apps are available to simplify the process, catering to various needs and technological preferences.

For those who prefer a simple, spreadsheet-based approach, Microsoft Excel or Google Sheets offer robust functionality. You can easily create custom worksheets to track income, expenses, and savings goals. The ability to create formulas and charts allows for in-depth analysis of your financial situation.

Alternatively, several dedicated budgeting apps offer user-friendly interfaces and automated features. Mint, for example, provides a comprehensive overview of your finances by connecting to your bank accounts and credit cards. It automatically categorizes transactions and provides insightful reports to help you identify areas for improvement. Other popular options include YNAB (You Need A Budget), known for its zero-based budgeting approach, and Personal Capital, which offers more advanced features like investment tracking.

Regardless of the tool or app you choose, remember that the key is consistency. Regularly updating your budget and reviewing your spending habits is crucial for achieving your financial goals. The best tool is the one that you find easiest to use and stick with consistently.

Adjust Monthly Based on Actual Use

One of the most crucial aspects of effective budgeting is regular review and adjustment. While a planned budget provides a solid framework, it’s essential to acknowledge that actual spending often deviates from initial projections.

At the end of each month, take some time to compare your planned budget against your actual spending. Categorize your expenses and analyze any significant differences. For example, if your grocery budget was significantly exceeded, examine your spending habits to identify areas for potential savings.

This process of comparison is vital for identifying trends and patterns in your spending. Are you consistently overspending in a particular category? Understanding these patterns allows you to make informed adjustments to your budget for the following month, ensuring that your budget remains a realistic and effective financial tool.

Flexibility is key. Your budget should not be a rigid, unyielding plan, but rather a dynamic document that adapts to your changing circumstances and spending habits. Don’t be afraid to make necessary adjustments, as this continuous refinement is a fundamental part of responsible financial management.

By consistently adjusting your monthly budget based on actual use, you gain a clearer picture of your financial situation, improve your financial forecasting accuracy, and ultimately enhance your chances of achieving your financial goals.

{kind=link}