Understanding your credit report is crucial for achieving your financial goals. A credit report is a detailed record of your credit history, impacting your ability to secure loans, rent an apartment, or even get a job. This comprehensive guide, “Understanding Your Credit Report in 6 Steps,” will equip you with the knowledge to navigate the complexities of your credit score and empower you to make informed financial decisions. Learn how to access your free annual credit reports, decipher the information presented, and identify potential errors that could be negatively affecting your creditworthiness.

Taking control of your credit report is a proactive step towards building a strong financial future. By following the six simple steps outlined in this article, you’ll gain a clear understanding of your credit standing, identify any potential issues, and learn how to improve your credit score over time. Whether you’re looking to buy a house, apply for a car loan, or simply want to improve your overall financial health, mastering your credit report is essential. Let’s begin your journey to credit literacy!

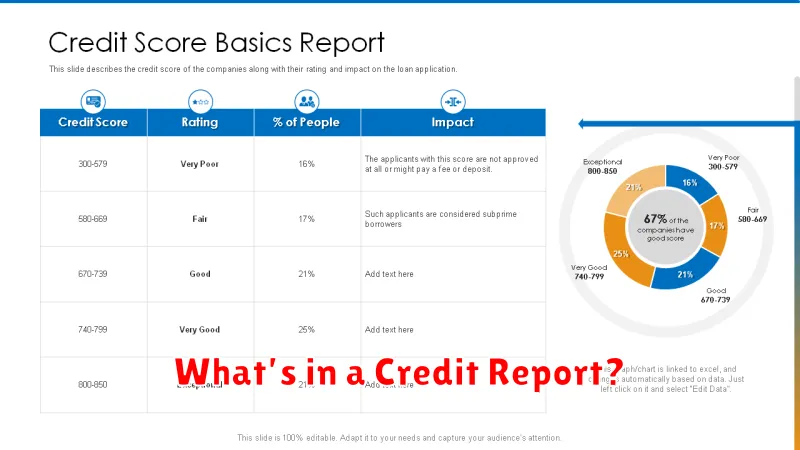

What’s in a Credit Report?

Your credit report is a detailed summary of your credit history, compiled by one of the three major credit bureaus: Equifax, Experian, and TransUnion. It’s a crucial document that lenders use to assess your creditworthiness when you apply for loans, credit cards, or other forms of credit.

The core components of your credit report include:

- Personal Information: This section contains your name, address, date of birth, and Social Security number. Accuracy is paramount; discrepancies can negatively impact your credit score.

- Credit Accounts: This is a comprehensive list of all your open and closed credit accounts, including credit cards, loans (auto, mortgage, personal), and other lines of credit. It will show your account balances, credit limits, payment history, and the dates the accounts were opened and closed.

- Payment History: This is arguably the most important part of your credit report. It details your payment history for all your credit accounts, noting any late or missed payments. Consistent on-time payments are vital for building and maintaining a good credit score.

- Public Records: This section includes information about any bankruptcies, foreclosures, tax liens, or judgments against you. These items can significantly impact your credit score and remain on your report for several years.

- Inquiries: This section lists any inquiries made by lenders or creditors to access your credit report. Too many inquiries in a short period can negatively affect your credit score, although some inquiries (like those related to rate shopping) have less of an impact.

Understanding the information contained within your credit report is essential for managing your finances effectively and ensuring your creditworthiness is accurately reflected. Regularly reviewing your report allows you to identify and correct any errors and track your progress toward improving your credit health.

How to Access It for Free

Accessing your credit report for free is a right guaranteed by the Fair Credit Reporting Act (FCRA). You’re entitled to a free copy from each of the three major credit bureaus – Equifax, Experian, and TransUnion – once every 12 months.

To obtain your free report, visit AnnualCreditReport.com. This is the only official website authorized by the FCRA to provide free credit reports. Beware of websites mimicking this address; they often charge fees or are scams.

The process on AnnualCreditReport.com is straightforward. You’ll need to provide some personal identifying information, including your name, address, Social Security number, and date of birth, to verify your identity. The site employs robust security measures to protect your data.

Once your identity is verified, you can select which credit bureau’s report you’d like to access. You can request a report from only one bureau at a time through this site. To get reports from all three bureaus, you’ll need to spread your requests over several months.

After submitting your request, you’ll typically receive your credit report within a few days via mail. You may also be able to access a digital version of your report directly on the site in some instances.

Remember, while your credit score is not included in the free report provided by AnnualCreditReport.com, the report provides the information lenders use to calculate your score. This allows you to monitor your credit health effectively.

What to Look for in Each Section

Understanding your credit report requires a careful review of each section. Accuracy is paramount; any errors can significantly impact your credit score. Begin by verifying your personal information – your name, address, and date of birth – ensuring everything is completely correct. Any discrepancies should be reported immediately to the credit bureau.

Next, scrutinize the accounts section. This lists all your credit accounts, including credit cards, loans, and mortgages. Carefully check the account numbers, dates opened, credit limits (for revolving credit), balances, and payment history. Disputes should be raised for any inaccuracies, such as late payments that weren’t made or accounts that aren’t yours.

The public records section details any bankruptcies, tax liens, or judgments against you. Review this information thoroughly, ensuring everything is accurate and properly reflects the legal proceedings. If you believe there are errors, challenge them with the appropriate documentation.

The inquiries section shows recent requests for your credit report. These are usually generated by lenders when you apply for credit. A high number of recent inquiries can slightly lower your credit score, so examine this section for any unauthorized inquiries that you should dispute. Be aware that some inquiries are considered “soft inquiries” and do not affect your score.

Finally, pay close attention to your credit score. This numerical representation summarizes your creditworthiness. Understand what factors contributed to your score and identify areas where improvement is needed. Remember that your credit report is a snapshot in time; your score can change over time as you manage your credit accounts responsibly.

Spotting Errors and Fraud

Reviewing your credit report for errors and signs of fraud is a crucial step in maintaining your financial health. Accuracy is paramount, as inaccuracies can negatively impact your credit score and ability to secure loans or credit cards.

Begin by carefully examining each account listed. Verify the account numbers, credit limits, and payment history. Check for any accounts you don’t recognize. Any discrepancies should be immediately flagged for further investigation. Pay close attention to dates; even a minor error in the date of an account opening or payment can be a sign of a larger problem.

Look for signs of identity theft. This might include accounts opened in your name that you didn’t authorize, addresses you don’t recognize, or inquiries from lenders you’ve never contacted. Unusual spending patterns on existing accounts can also indicate fraudulent activity. Be particularly vigilant about any accounts with unusually high balances or frequent late payments.

If you discover any errors or suspect fraud, promptly contact the credit reporting agency (CRA) and the creditor involved. Each CRA has a process for disputing inaccurate information, typically involving submitting a written dispute letter. Document all communication and retain copies of any supporting evidence. Remember to contact the relevant authorities if you believe you are a victim of identity theft.

Addressing errors and fraudulent activity swiftly is essential. The sooner you identify and rectify these issues, the less impact they will have on your creditworthiness. Your diligence in reviewing your credit report and taking prompt action can save you significant financial hardship in the long run.

How to Dispute Mistakes Correctly

Disputing inaccuracies on your credit report is a crucial step in maintaining a healthy credit profile. Accuracy is paramount, as errors can negatively impact your credit score and ability to secure loans or favorable interest rates. To effectively dispute, follow these guidelines.

First, you need to obtain a copy of your credit report from each of the three major credit bureaus: Equifax, Experian, and TransUnion. Carefully review each report for any discrepancies. This includes checking for incorrect personal information, such as your name, address, or social security number, as well as inaccurate account information, like late payments or accounts that don’t belong to you. Documentation is key; gather any evidence that supports your claim, such as payment receipts, bank statements, or copies of contracts.

Next, submit a formal dispute letter to each bureau individually. Use certified mail with return receipt requested to confirm delivery and maintain a record of your correspondence. The letter should clearly state the specific errors you’ve identified, providing detailed supporting documentation. Be concise and factual, avoiding emotional language or accusations. Each credit bureau has a specific address for dispute letters; ensure you use the correct one.

After submitting your dispute, the credit bureau is required to investigate your claim. This process typically takes 30-45 days. During this period, you may receive updates on the progress of your investigation. Once the investigation is complete, the bureau will either correct the error, or provide a written explanation as to why they believe the information is accurate. If the error is not corrected, you may need to consider further action, possibly involving the Consumer Financial Protection Bureau (CFPB).

Remember to keep meticulous records of all your correspondence, including copies of your dispute letters, supporting documents, and any communication received from the credit bureaus. This documentation will be essential should you need to escalate your dispute or take further legal action. Persistence and careful attention to detail are crucial in successfully resolving credit report errors.

How Often You Should Check

Checking your credit report regularly is crucial for maintaining good financial health. The frequency with which you do so depends on your individual circumstances, but a good rule of thumb is to review your report at least once a year.

If you’re planning a major purchase, such as a house or car, it’s especially important to check your report several months in advance. This allows you time to identify and address any errors or discrepancies that could impact your ability to secure favorable financing terms.

For individuals with complex financial situations, or those who have recently experienced identity theft or fraud, more frequent monitoring—perhaps every three to four months—might be warranted. This proactive approach helps ensure early detection of any suspicious activity.

Beyond these specific scenarios, simply reviewing your report annually offers a valuable snapshot of your creditworthiness and allows you to track your progress over time. Regular monitoring empowers you to take corrective action if needed and maintain a positive credit history.

{kind=link}