Improving your credit score can feel like a daunting task, but with a structured approach and consistent effort, you can achieve a significant improvement. This step-by-step guide provides actionable strategies to boost your creditworthiness and unlock better financial opportunities. We’ll cover essential areas like understanding your credit report, managing debt effectively, and establishing a positive payment history, ultimately helping you reach your desired credit score range. Learning how to improve credit score is an investment in your financial future, paving the way for lower interest rates on loans, better terms on credit cards, and improved access to financial products.

This comprehensive guide outlines practical steps to build credit or repair credit, regardless of your current credit score. We will demystify the credit scoring process, explaining the factors that contribute to your overall score and providing clear, actionable advice for each. Whether you’re looking to qualify for a mortgage, secure a personal loan, or simply achieve better financial health, mastering these credit repair techniques can significantly impact your financial well-being. Understanding your credit report and proactively managing your credit are key to achieving a higher credit score and securing a brighter financial future.

Understand the Five Score Factors

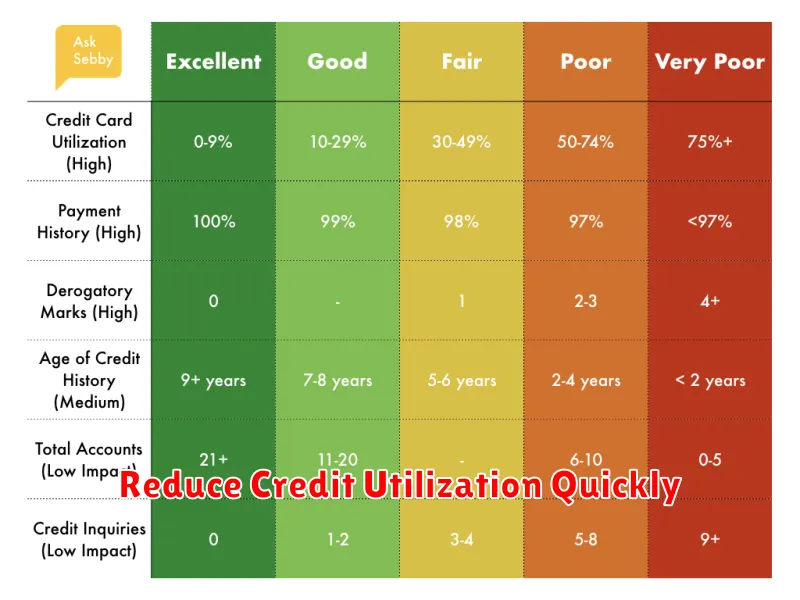

Your credit score, a crucial element in securing loans and financial products, is determined by five key factors. Understanding these factors is the first step towards improving your creditworthiness. These five factors are weighted differently by various credit scoring models, but their overall importance remains consistent.

Payment History is the most significant factor, typically accounting for 35% of your score. This reflects your consistency in making on-time payments on all your credit accounts, including credit cards, loans, and mortgages. Even a single missed payment can negatively impact your score. Consistent on-time payments are vital for a healthy credit profile.

Amounts Owed, representing 30% of your score, focuses on your credit utilization ratio. This is the percentage of your available credit that you’re currently using. Keeping your credit utilization low, ideally below 30%, significantly benefits your score. Carrying high balances on your credit cards indicates a higher level of debt, signaling greater risk to lenders.

Length of Credit History accounts for 15% of your score. This refers to the age of your oldest and average credit accounts. A longer credit history demonstrates a proven track record of responsible credit management. Avoid closing older accounts unless absolutely necessary, as this can negatively impact the average age of your credit history.

New Credit comprises 10% of your score and reflects the number of new credit accounts you’ve opened recently. Opening multiple new accounts in a short period suggests increased risk to lenders. Limit the number of credit applications you submit within a given timeframe.

Credit Mix, the final 10% factor, considers the variety of credit accounts you possess. Having a mix of credit card accounts, installment loans (like car loans or personal loans), and mortgages can demonstrate a broader understanding and management of different credit types. While a diverse credit mix is beneficial, it’s less important than the other four factors.

Pay on Time Every Month

One of the most crucial factors influencing your credit score is your payment history. Credit bureaus meticulously track your payment patterns, and even a single missed payment can significantly impact your score. Making on-time payments consistently demonstrates your financial responsibility and reliability to lenders.

To ensure timely payments, consider setting up automatic payments. Many credit card companies and loan providers offer this convenient feature, which automatically deducts your payment from your checking account on the due date. This eliminates the risk of forgetting or missing a payment due to oversight.

Another helpful strategy is to create a payment calendar. This can be a simple spreadsheet or a digital calendar that lists all your monthly bills and their due dates. This allows you to plan your finances effectively and avoid late payments by proactively managing your budget and upcoming expenses.

If you anticipate potential difficulties meeting a payment deadline, it’s essential to contact your creditor immediately. Many lenders are willing to work with you to arrange a payment plan or explore other options to prevent a missed payment from negatively affecting your credit report. Proactive communication demonstrates responsibility and can mitigate potential damage to your credit score.

Remember, consistent on-time payments are fundamental to building and maintaining a strong credit history. By adopting these strategies and remaining diligent, you’ll significantly increase your chances of achieving a favorable credit score.

Reduce Credit Utilization Quickly

One of the most impactful ways to improve your credit score is to reduce your credit utilization ratio. This ratio represents the percentage of your available credit that you’re currently using. Lenders view a high utilization ratio as a sign of potential financial instability, negatively affecting your credit score.

To quickly reduce your credit utilization, consider making a significant payment on your credit cards. Even paying off a portion of your balances can make a noticeable difference. Aim to keep your utilization ratio below 30%, ideally below 10%, for optimal credit health. The lower, the better.

Another effective strategy involves requesting a credit limit increase from your credit card issuers. This increases your available credit, thereby lowering your utilization ratio without changing your outstanding balance. However, be mindful that requesting too many increases in a short period can sometimes negatively impact your credit score, so proceed cautiously.

If you have multiple credit cards with low credit limits, it might be beneficial to consolidate your debt. This can be done by transferring balances to a card with a higher credit limit or through a debt consolidation loan. Remember to compare fees and interest rates carefully before making any decisions.

Finally, avoid opening new credit accounts unless absolutely necessary while you’re working on improving your credit utilization. Each new account causes a slight, temporary dip in your score and can temporarily raise your utilization ratio as your available credit increases before you pay off what you’ve bought.

Avoid New Inquiries Too Often

One crucial factor influencing your credit score is the number of recent credit inquiries. Each time a lender checks your credit report, it’s recorded as a hard inquiry, and multiple hard inquiries within a short period can negatively impact your score. This is because lenders view numerous inquiries as a sign of potential financial risk, suggesting you might be struggling to manage your finances or are overextending yourself with debt.

While some inquiries, such as those when you’re comparison shopping for loans or credit cards, might be grouped together by credit bureaus and considered a single inquiry, it’s still wise to limit the number of applications you submit. Space out your applications to avoid an unnecessary ding to your credit score. Consider your need for new credit carefully before submitting an application. Do you truly need another credit card or loan at this time?

It’s important to remember that even pre-approved credit offers can trigger a hard inquiry on your credit report, impacting your score. Carefully weigh the potential benefits of new credit against the potential short-term negative impact on your credit score. Focusing on improving your existing credit utilization and payment history will generally yield a more significant and sustainable positive effect on your creditworthiness than repeatedly applying for new credit.

Build Long-Term Credit History

Establishing a long-term credit history is crucial for a strong credit score. Lenders look favorably upon individuals with a consistent and lengthy track record of responsible credit management. This demonstrates your reliability and ability to handle financial obligations over time.

One of the most effective ways to build credit history is by obtaining and responsibly managing a credit card. Make sure to pay your balance in full and on time each month, avoiding any late payments. This consistent, on-time payment history is a key factor in improving your credit score.

Another strategy is to become an authorized user on a credit card account held by someone with a good credit history. If the primary cardholder maintains a positive payment record, this positive activity can be reflected on your credit report, helping build your own credit history. However, be aware that this method relies heavily on the responsible actions of the primary account holder.

Beyond credit cards, consider taking out a small loan, such as a personal loan or a loan for a small purchase. Again, consistent on-time payments are vital. Successfully repaying these loans demonstrates your creditworthiness to lenders.

Maintaining a variety of credit accounts, including both revolving credit (like credit cards) and installment credit (like loans), can also be beneficial. This demonstrates your ability to manage different types of credit responsibly. However, avoid opening too many accounts in a short period, as this could negatively impact your score.

Regularly monitoring your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) is essential to ensure accuracy and identify any potential issues. Early detection of errors allows for timely correction, protecting your credit history.

Monitor Your Report Regularly

Regularly reviewing your credit report is crucial for maintaining a healthy credit score. By doing so, you can proactively identify and address any potential issues before they negatively impact your score. Errors, such as incorrect account information or fraudulent activity, can significantly lower your score, and early detection is key to resolving them quickly.

You are entitled to a free credit report annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion). Take advantage of this resource and schedule a review at least once a year. This allows you to catch inaccuracies or suspicious activity promptly. Consider spreading your requests throughout the year (one report every four months) to get a more comprehensive overview.

Beyond simply looking for errors, monitoring your report also helps you track your credit utilization. This refers to the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (ideally below 30%) is a significant factor in determining your credit score. Regular checks allow you to see if you’re approaching or exceeding this threshold, prompting you to adjust your spending habits accordingly.

Finally, reviewing your report helps you stay informed about your credit history. Understanding your payment patterns, account types, and length of credit history allows you to make informed decisions to further improve your creditworthiness. This might involve paying down debt, applying for new credit strategically, or taking steps to improve your payment history.

{kind=link}