Are you overwhelmed by debt? Do you feel trapped by high-interest rates and minimum payments that barely make a dent? Many struggle with the burden of credit card debt, student loans, and other forms of personal debt, but there’s hope. This article breaks down the debt snowball method, a popular and effective strategy for paying off debt faster and regaining financial control. Learn how this proven technique can help you conquer your debts and achieve financial freedom.

The debt snowball method is a behavioral approach to debt repayment, prioritizing psychological momentum over mathematical optimization. Unlike the debt avalanche method, which focuses on paying off the highest-interest debt first, the snowball method emphasizes paying off the smallest debt first, regardless of interest rate. This creates a sense of accomplishment and motivates you to continue the process, building momentum as you “snowball” your way to becoming debt-free. This article will explore the advantages and disadvantages of this method, providing you with the knowledge to determine if it’s the right choice for your financial situation.

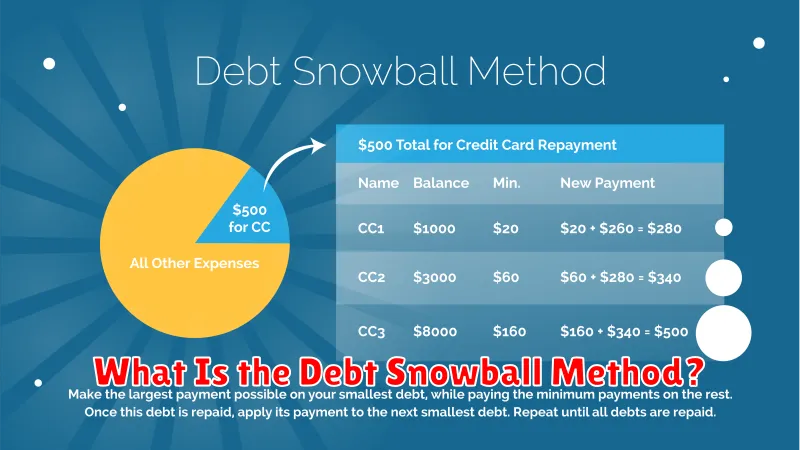

What Is the Debt Snowball Method?

The debt snowball method is a popular debt repayment strategy that prioritizes paying off debts based on their balance size, rather than interest rate. It focuses on building momentum and motivation by tackling smaller debts first.

Instead of focusing on the interest rate, which is the approach of the debt avalanche method, the debt snowball method concentrates on the balance of each debt. You list all your debts from smallest to largest balance, regardless of their interest rates. You then aggressively pay off the smallest debt while making minimum payments on all other debts.

Once the smallest debt is paid off, you take that payment amount and add it to the payment you’re making on the next smallest debt. This creates a “snowball” effect, rapidly increasing your payment amount as you pay off each successive debt. This process continues until all debts are eliminated.

The psychological benefit of this method is significant. Seeing quick wins early on through paying off smaller debts can provide a boost in motivation and help maintain consistency throughout the repayment process. This psychological advantage can be crucial for those struggling with debt and needing encouragement to stay the course.

However, it’s important to note that because it prioritizes balance over interest rate, the debt snowball method may not be the most financially efficient strategy in the long run. You might end up paying more in interest compared to the debt avalanche method. The choice between the two depends largely on individual preferences and psychological needs.

Why It Works for Motivation

The debt snowball method’s power lies in its psychological impact, not just its mathematical efficiency. While other methods might offer faster overall debt reduction, the snowball method excels at maintaining momentum and fostering a sense of accomplishment.

The strategy focuses on paying off the smallest debt first, regardless of interest rate. This early, quick win provides a significant psychological boost. Seeing that first debt eliminated fuels motivation and reinforces the positive behavior of consistent repayment. This early success builds confidence, making it easier to tackle larger debts later.

The snowball effect is not just a metaphor; it’s a self-perpetuating cycle. Each small victory generates excitement and encourages even greater effort in the following stages. The feeling of progress, however incremental it might seem at the start, is a powerful motivator that keeps individuals engaged and committed to the long-term goal of becoming debt-free.

Furthermore, the visual representation of progress is crucial. As each debt is paid off, the individual can visually remove it from their list or tracking system. This visual progress provides a constant reminder of the positive movement and fuels further determination.

In essence, the debt snowball method leverages the power of positive reinforcement and psychological momentum to overcome the often-overwhelming feeling of being buried under debt. It’s a method designed to foster intrinsic motivation, leading to consistent effort and ultimately, financial freedom.

How to List and Organize Your Debts

Before you can begin tackling your debts using the debt snowball method, you need a clear understanding of your financial landscape. This starts with creating a comprehensive list of all your outstanding debts. Be meticulous; include every single debt, no matter how small it seems.

Organize your list by creating a table or spreadsheet. This will make it much easier to manage and track your progress. Include the following key information for each debt:

- Creditor Name: The name of the company or individual you owe money to.

- Account Type: Specify whether it’s a credit card, loan (personal, auto, student, etc.), medical bill, or other.

- Current Balance: The total amount you currently owe.

- Minimum Payment: The minimum amount required to avoid late fees.

- Interest Rate: The annual percentage rate (APR) charged on the outstanding balance. This is crucial for understanding the cost of your debt.

Once you’ve compiled this information, you can begin to prioritize your debts based on the debt snowball method. This involves focusing on the smallest debt first, regardless of its interest rate, to build momentum and motivation. Accurate listing and organization is the foundation of success with this strategy.

Consider using budgeting software or a spreadsheet program to help manage this data. These tools can automate calculations and provide visual representations of your debt, making the process more efficient and less daunting. The accuracy of this initial step is critical for effective debt management.

What to Do After Paying the First One Off

Once you’ve successfully paid off your smallest debt, a sense of accomplishment should wash over you. This is a major milestone in your debt-free journey. However, don’t let the victory lead to complacency. Maintaining momentum is crucial to continued success.

The next step is to immediately roll that monthly payment amount into your next smallest debt. This is the core principle of the debt snowball method: snowballing your payments to accelerate progress. Don’t allocate the funds elsewhere; instead, redirect them to rapidly decrease your next debt balance. You will quickly see the results of this strategic move.

While celebrating your progress is important, it’s equally important to maintain your budget and spending habits. Stick to the financial discipline that allowed you to pay off the first debt. This consistency will prove invaluable as you tackle larger debts in the coming months.

Consider reviewing your budget. With one debt eliminated, you might have some breathing room. Analyze whether you can increase your payments on the next debt. Even a small increase will have a significant impact over time. Alternatively, you may wish to allocate extra funds toward building an emergency fund to further fortify your financial security.

Remember, patience and perseverance are vital. The debt snowball method may take time, but the feeling of accomplishment after each payment is a powerful motivator. Stay focused on your goal, and celebrate each win along the way. The feeling of freedom that comes with being debt-free is worth the effort.

Common Mistakes People Make

One of the most frequent errors is underestimating the time commitment required. The debt snowball method demands consistent effort and discipline. Many individuals begin enthusiastically, but falter when faced with unexpected expenses or lifestyle changes.

Another common pitfall is failing to track progress accurately. Without meticulous record-keeping, it’s difficult to monitor your progress and stay motivated. A detailed budget and regular updates are crucial for success.

Many individuals struggle with maintaining focus on the snowball. The allure of quick financial fixes or tempting purchases can derail the entire process. Remember that the method’s success hinges on unwavering commitment to the plan.

A significant mistake is ignoring interest rates. While the emotional satisfaction of paying off smaller debts first is undeniable, prioritizing debts with the highest interest rates can ultimately save you a considerable amount of money over time. A balanced approach that considers both emotional and financial factors is ideal.

Finally, some people make the mistake of not adjusting their budget as needed. Life throws curveballs, and unexpected expenses happen. It’s essential to regularly review and adjust your budget to account for unforeseen circumstances and ensure you remain on track.

When to Switch to Avalanche Method

While the debt snowball method focuses on the psychological benefits of quickly paying off smaller debts, the avalanche method prioritizes financial efficiency. The avalanche method tackles debts with the highest interest rates first, regardless of balance size. This ultimately saves you money in the long run by minimizing the total interest paid.

Consider switching to the avalanche method when:

- High-interest debt is significantly impacting your overall financial health. The interest accumulating on these debts outweighs the motivational benefits of the snowball method.

- You have a stronger financial foundation and can handle the potential emotional challenges of focusing on larger, higher-interest debts before smaller ones.

- You are comfortable with a more calculated and analytical approach to debt repayment, prioritizing mathematical efficiency over the immediate gratification of the snowball method.

- You are disciplined enough to stick with a potentially longer repayment plan, as the avalanche method might take longer to see initial wins compared to the snowball.

Ultimately, the best method depends on your individual financial situation and personality. The key is to choose a method you can stick with consistently to achieve your debt-free goals.

{kind=link}