Are you working harder but feeling like you’re not getting ahead? You might be experiencing lifestyle inflation, the insidious phenomenon where your spending habits rise in line with your income. This seemingly harmless trend can trap you in a cycle of debt and prevent you from achieving your financial goals, such as saving for retirement or buying a home. Learning how to avoid lifestyle inflation is crucial for building lasting wealth and securing your financial future. This article will provide practical strategies to help you break free from this common trap and take control of your finances.

Understanding the mechanics of lifestyle inflation is the first step towards combating it. It’s not simply about spending more; it’s about unconsciously adjusting your spending habits to match your increased income, often leading to a feeling of being perpetually broke despite earning more. We’ll explore the subtle ways lifestyle inflation creeps in, from upgrading your daily coffee to purchasing a more expensive car. By identifying your spending triggers and implementing effective budgeting techniques, you can successfully manage your finances and achieve true financial freedom. This guide will empower you to make informed decisions about your money and build a sustainable path towards financial security.

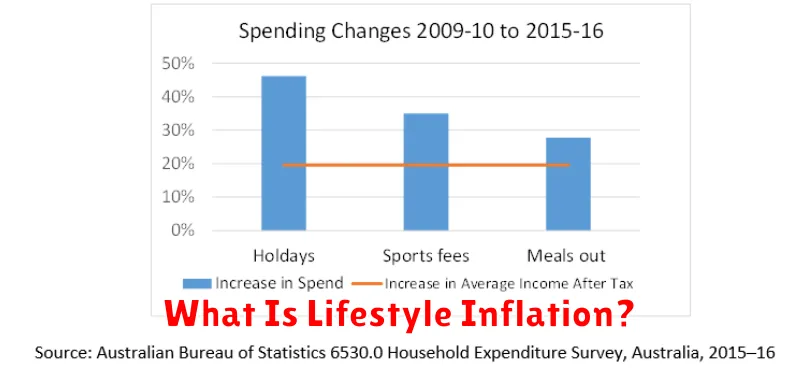

What Is Lifestyle Inflation?

Lifestyle inflation refers to the tendency to increase one’s spending as one’s income rises. It’s the insidious habit of upgrading your lifestyle to match your increased earnings, rather than saving or investing a larger portion of that increase.

Instead of viewing a pay raise as an opportunity to boost savings and accelerate financial goals, individuals experiencing lifestyle inflation use the extra money to acquire more expensive goods and services, often without careful consideration of their long-term financial implications. This can manifest in various ways, from purchasing a more luxurious car or upgrading to a larger home, to indulging in more frequent expensive meals and vacations.

The key element is that the spending increases are not necessarily essential; rather, they are driven by a desire for a higher standard of living proportional to the increased income. This can lead to a vicious cycle where, despite earning more, individuals feel no more financially secure because their spending habits have grown in tandem.

The impact of lifestyle inflation can be substantial. It can hinder progress towards financial goals like retirement planning, debt reduction, and investing. By continually adjusting spending to match income, opportunities to build wealth and achieve financial freedom are significantly reduced.

Understanding lifestyle inflation is crucial for developing sound financial habits. Recognizing this tendency is the first step in breaking the cycle and building a more secure financial future.

Recognizing Spending Triggers

Understanding your spending triggers is crucial to combating lifestyle inflation. These are the situations, emotions, or environments that prompt you to spend money, often impulsively and without careful consideration.

Common triggers include stress. When feeling overwhelmed, many individuals turn to retail therapy as a temporary escape, leading to unnecessary purchases. Similarly, boredom can lead to impulsive online shopping sprees or dining out.

Social pressure is another significant trigger. The desire to keep up with peers or meet societal expectations can drive excessive spending on items like clothing, electronics, or experiences. Consider the impact of marketing and advertising; cleverly crafted campaigns designed to evoke emotions and encourage immediate purchasing decisions.

Positive emotions can also be spending triggers. Celebrations, achievements, or even a good mood might prompt lavish purchases, blurring the lines between deserved rewards and overspending. Conversely, negative emotions such as sadness or anxiety can fuel impulsive buying as a coping mechanism.

Convenience plays a role as well. Easy access to online shopping and readily available credit options lower the barriers to spending, making it simpler to make impulsive purchases. Recognizing these various triggers – from emotional states to environmental factors – is the first step towards gaining control over your spending habits.

Why More Income ≠ More Spending

The common assumption that increased income automatically translates to increased spending is a dangerous misconception fueling lifestyle inflation. While a higher salary provides more financial breathing room, it doesn’t inherently dictate a proportional rise in expenses. The crucial distinction lies in conscious financial management and deliberate spending choices.

Lifestyle inflation occurs when your spending habits adjust to match your income, negating the benefits of a salary increase. You might find yourself upgrading to a more expensive car, moving to a larger home, or indulging in more frequent luxury purchases. This pattern creates a vicious cycle: the more you earn, the more you spend, leaving you no better off financially than before, and often worse off due to increased debt.

The key to avoiding this trap is to maintain a clear separation between your income increase and your spending habits. Treat any additional income as an opportunity to bolster your savings, invest wisely, or accelerate your debt repayment. Instead of automatically adjusting your lifestyle, consciously decide which expenditures truly add value and which are simply fleeting pleasures.

A budget is invaluable in this process. By meticulously tracking your income and expenses, you can identify areas where you’re overspending and prioritize essential needs over superfluous wants. This awareness enables informed decision-making, ensuring that your increased income serves your long-term financial goals rather than fueling unsustainable spending patterns.

Remember, financial freedom isn’t about earning more, but about spending less relative to your earnings. A higher income offers the potential for greater financial security and wealth accumulation, but only if managed effectively. By consciously resisting the temptation of lifestyle inflation, you can leverage your increased income to build a stronger financial future.

How to Set Lifestyle Boundaries

Avoiding lifestyle inflation requires a conscious effort to set boundaries around your spending habits. This means defining what constitutes a “need” versus a “want” and sticking to that distinction. Begin by honestly assessing your current spending. Track your expenses for a month to identify areas where your spending exceeds your income or your comfort level. This will illuminate where you might be susceptible to lifestyle creep.

Next, create a budget that reflects your values and financial goals. Prioritize essential expenses like housing, food, transportation, and healthcare. Allocate funds for savings and debt repayment. Only after covering these necessities should you consider discretionary spending. Consider using budgeting apps or spreadsheets to facilitate this process and track your progress.

A key element of setting boundaries is learning to say no. This applies to both large purchases and smaller indulgences. Before making a purchase, ask yourself if it truly aligns with your budget and your overall financial goals. If it doesn’t, politely decline. This might involve saying no to social outings that strain your finances or resisting the urge to keep up with the latest trends.

Consider establishing a waiting period before making significant purchases. This allows time for careful consideration and prevents impulsive buying decisions. This period could range from a few days to several weeks, depending on the size and importance of the purchase. This simple strategy can significantly reduce lifestyle inflation.

Finally, cultivate mindfulness in your spending habits. Regularly review your budget and expenses to ensure you’re staying on track. Be aware of the emotional triggers that might lead to overspending, and develop strategies to manage them. By being mindful and intentional with your finances, you can effectively set and maintain lifestyle boundaries.

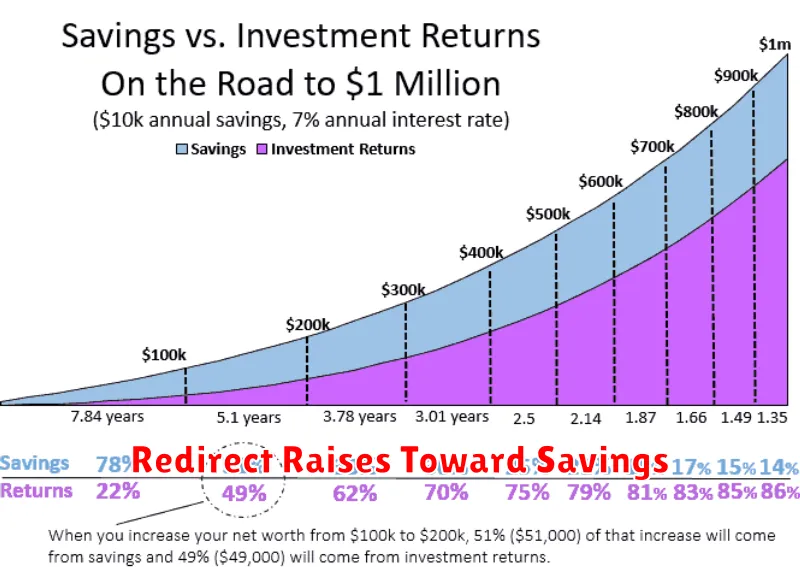

Redirect Raises Toward Savings

One of the biggest challenges in avoiding lifestyle inflation is the tendency to automatically increase spending as income rises. This is often referred to as a “lifestyle creep.” Instead of viewing a raise as purely disposable income, redirect a significant portion of that increased income directly into your savings goals.

Consider this a form of pre-committed saving. Before you even think about how you’ll spend the extra money, allocate a percentage — ideally a significant one — toward your savings or debt reduction plan. This prevents the temptation to adjust your lifestyle to match the higher income level.

A practical strategy is to treat the raise as if it never happened, at least initially. Maintain your current spending habits for a period of time, then gradually increase spending only after you’ve had a chance to build up your savings. This disciplined approach ensures that your increased income works for you, not the other way around.

Determine how much of your raise you want to dedicate to savings, factoring in your current savings goals, emergency fund, and long-term aspirations. This may involve setting up automatic transfers from your checking account to a savings or investment account. The automation is key; it prevents you from having to actively make the decision each month, decreasing the likelihood of succumbing to the allure of immediate gratification.

Remember, the goal is to increase your net worth, not just your spending power. By strategically redirecting raises toward savings, you’ll build a more secure financial future and effectively mitigate the negative impacts of lifestyle inflation.

Reward Yourself Without Overspending

Lifestyle inflation, the tendency to increase spending as income rises, is a common pitfall. It’s easy to fall into the trap of justifying bigger purchases because you can now “afford” them. However, financial well-being requires mindful spending habits, even with increased income. This doesn’t mean denying yourself pleasures; it means finding creative ways to reward yourself without breaking the bank.

Instead of immediately upgrading to a more expensive car or moving to a larger home, consider smaller, more sustainable rewards. Think about experiences rather than material possessions. A weekend getaway to a nearby state park, a concert with friends, or a cooking class can provide lasting memories and a sense of fulfillment without significant financial strain. These experiences often offer a greater return on your investment in happiness than expensive material goods.

Prioritize experiences over possessions. Research shows that experiences tend to bring greater long-term happiness than material purchases. This is because experiences create lasting memories and personal growth, unlike material possessions that can lose their novelty quickly. Therefore, shifting your focus towards experiences provides a more sustainable path to rewarding yourself.

Set a realistic budget for rewards. Allocate a specific amount each month for rewarding yourself. This prevents impulsive spending and keeps your rewards aligned with your overall financial goals. Sticking to a budget allows you to enjoy your rewards without compromising your long-term financial stability.

Explore free or low-cost activities. Many rewarding activities don’t require significant spending. Consider free outdoor activities like hiking, biking, or exploring your city. Take advantage of free events in your community or visit museums on their free admission days. These activities can provide just as much, if not more, satisfaction than expensive outings.

By consciously choosing fulfilling experiences and setting a budget, you can effectively reward yourself without succumbing to lifestyle inflation and maintain a healthy relationship with your finances. Remember, the key is to find a balance between enjoying life’s pleasures and maintaining financial responsibility.

{kind=link}