Are you struggling to manage your finances effectively and achieve your financial goals? Do you find yourself constantly wondering where your money goes each month? Then understanding the 50/30/20 budget rule is crucial. This simple yet powerful budgeting method can help you gain control of your spending, build a strong financial foundation, and work towards financial freedom. It’s a practical framework that divides your after-tax income into three clear categories: needs, wants, and savings, empowering you to make informed financial decisions and track your progress effortlessly.

The 50/30/20 rule offers a straightforward approach to personal finance management, enabling you to allocate your income strategically. By following this proven budgeting technique, you’ll be able to prioritize essential expenses, indulge in occasional wants without guilt, and consistently save for your future financial security. This article will delve into the specifics of each category, providing practical tips and examples to help you successfully implement the 50/30/20 budget rule and achieve your personal financial objectives. Learn how to effectively budget your income and pave the way towards a more secure financial future.

What Is the 50/30/20 Rule?

The 50/30/20 rule is a simple yet effective personal finance guideline that suggests allocating your after-tax income across three categories: needs, wants, and savings.

Specifically, the rule recommends allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

Needs encompass essential expenses such as housing, utilities, groceries, transportation, healthcare, and debt payments (minimum payments only). These are expenditures crucial for maintaining your basic standard of living.

Wants represent non-essential expenses, those things you enjoy but aren’t strictly necessary for survival. This category includes dining out, entertainment, travel, subscriptions, and hobbies.

Finally, savings and debt repayment constitutes the remaining 20%. This portion should be allocated towards building an emergency fund, paying down high-interest debt, and saving for long-term goals like retirement or a down payment on a house. Prioritizing high-interest debt repayment is crucial here.

It’s important to note that the 50/30/20 rule is a guideline, not a rigid prescription. The exact percentages may need adjustment based on individual circumstances and financial goals. For example, individuals with significant student loan debt might allocate a higher percentage to debt repayment initially.

Breakdown: Needs, Wants, Savings

The 50/30/20 budget rule is a simple yet effective tool for managing your finances. It divides your after-tax income into three categories: needs, wants, and savings.

Needs represent the essential expenses required for survival and well-being. This category typically includes housing (rent or mortgage payments), utilities (electricity, water, gas), groceries, transportation (car payments, gas, public transport), healthcare (insurance premiums, medical bills), debt repayments (minimum payments on loans), and childcare expenses. The goal is to allocate 50% of your after-tax income to cover these essential needs.

Wants are the non-essential expenses that improve your quality of life but aren’t necessary for survival. This category encompasses things like dining out, entertainment (movies, concerts), subscriptions (streaming services, gym memberships), new clothes, and hobbies. The 50/30/20 rule suggests allocating 30% of your income to wants. It’s crucial to be mindful of spending in this area to avoid overspending and maintain financial stability.

Savings are crucial for future financial security and achieving long-term goals. This includes emergency funds (covering unexpected expenses), retirement savings, down payments on a house or car, or investments. The 50/30/20 rule recommends allocating 20% of your after-tax income towards savings. Building a solid savings foundation is essential for mitigating financial risks and accomplishing your financial objectives.

How to Apply It to Any Income

The 50/30/20 budget rule is incredibly versatile and adaptable to various income levels. Its power lies in its proportional nature, not fixed dollar amounts. Instead of focusing on specific numbers, concentrate on the percentages.

To apply it to your income, first determine your monthly net income (income after taxes and deductions). Let’s say your net monthly income is $3,000. Now, calculate the amounts for each category:

- Needs (50%): $3,000 x 0.50 = $1,500. This covers essential expenses like rent/mortgage, utilities, groceries, transportation, and debt payments.

- Wants (30%): $3,000 x 0.30 = $900. This includes dining out, entertainment, hobbies, and non-essential shopping.

- Savings & Debt Repayment (20%): $3,000 x 0.20 = $600. This is allocated to savings, retirement contributions, and paying down debt aggressively.

If your income is lower, say $1,500, the percentages remain the same: 50% for needs ($750), 30% for wants ($450), and 20% for savings and debt repayment ($300). The absolute dollar amounts will change, but the proportional allocation ensures you’re consistently prioritizing your financial well-being.

Similarly, with a higher income, the amounts increase proportionally. The key is to maintain the 50/30/20 ratio regardless of income fluctuations. This consistency fosters good financial habits and helps you manage your money effectively at any income level.

Remember, this is a guideline. You may need to adjust the percentages based on your specific circumstances and financial goals. For example, if you have significant debt, you might allocate a larger percentage (more than 20%) to debt repayment temporarily.

Pros and Cons of the Method

The 50/30/20 budget rule offers a simple yet effective framework for managing personal finances. However, like any budgeting method, it has its advantages and disadvantages.

Pros: One of the biggest advantages is its simplicity. The straightforward allocation of funds makes it easy to understand and implement, even for those with limited financial literacy. This clarity allows for quick budgeting and better tracking of spending habits. Furthermore, the emphasis on saving 20% of income fosters a strong savings habit, crucial for long-term financial goals like retirement or emergency funds. The flexible nature of the 30% allocated to wants allows for personal adjustments based on individual priorities and lifestyle choices.

Cons: A potential drawback is its lack of personalization. The fixed percentages may not suit everyone’s unique financial situation and spending patterns. Individuals with higher debts or unexpected expenses might find the 20% savings target difficult to achieve. The rule also doesn’t explicitly account for debt repayment, which might require a higher percentage allocation depending on the individual’s circumstances. Finally, accurately tracking spending within the allocated percentages requires discipline and consistent monitoring, which some individuals may find challenging.

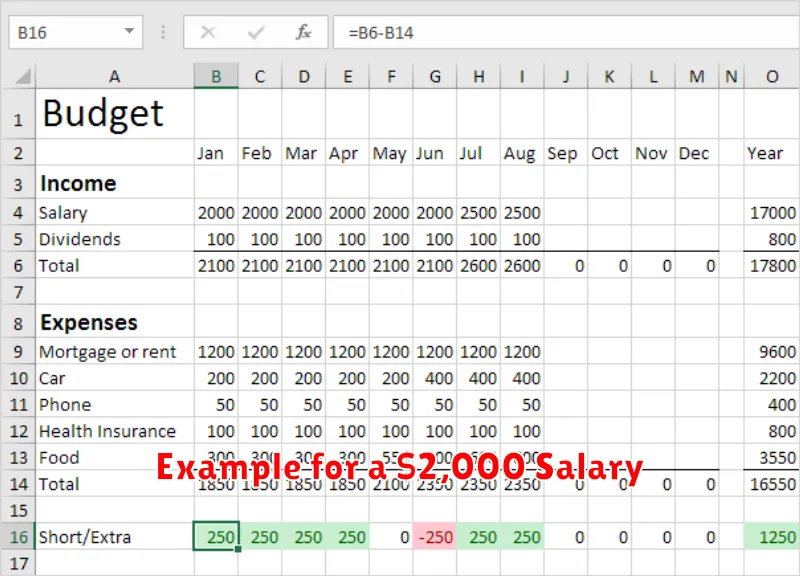

Example for a $2,000 Salary

Let’s illustrate the 50/30/20 budget rule with a concrete example using a $2,000 monthly salary. This breakdown will show how to allocate funds effectively across needs, wants, and savings.

Needs (50%): This category covers essential expenses necessary for survival and maintaining a stable life. For a $2,000 salary, 50% equates to $1,000. This allocation might include:

- Housing: $500 (rent or mortgage payment)

- Utilities: $150 (electricity, water, gas, internet)

- Transportation: $100 (car payment, gas, public transportation)

- Groceries: $150 (food and household supplies)

- Healthcare: $100 (insurance premiums, medical expenses)

Note: These figures are examples and will vary greatly based on individual circumstances and location.

Wants (30%): This portion encompasses non-essential spending, contributing to quality of life and personal enjoyment. With a $2,000 salary, this amounts to $600. This could include:

- Dining Out: $100

- Entertainment: $150 (movies, concerts, hobbies)

- Clothing: $100

- Personal Care: $50

- Subscriptions: $200 (streaming services, gym memberships)

Note: Adjust these amounts based on your personal preferences and spending habits.

Savings (20%): This crucial segment prioritizes financial security and future goals. For a $2,000 salary, this represents $400. This could be allocated to:

- Emergency Fund: $200 (building a safety net for unexpected expenses)

- Retirement Savings: $100 (contributing to a 401k or IRA)

- Debt Repayment: $100 (paying down credit card debt or loans)

Note: The distribution within savings depends on individual financial priorities and goals.

When to Adjust the Ratio

The 50/30/20 rule is a helpful guideline, but it’s not a rigid formula. Life circumstances change, and your budget should adapt accordingly. There will be times when adjusting the ratio is necessary to meet your financial goals and maintain a healthy financial life.

You might need to increase your savings rate (20%) during periods of financial uncertainty, such as job loss or unexpected medical expenses. This could involve temporarily reducing your spending in other categories. Similarly, if you have a significant debt burden, you might allocate a larger portion of your income towards debt repayment, even if it means temporarily reducing the amount you save or spend on wants.

Conversely, you may find that you can increase your spending on needs (50%) or wants (30%) if your income increases significantly or you pay off a large debt. This adjustment should be made cautiously, however, ensuring that you still maintain a comfortable savings rate and don’t fall into the trap of increased spending outpacing increased income.

Life events such as marriage, having children, or buying a home will almost certainly require adjustments to the 50/30/20 ratio. These events often involve significant shifts in both income and expenses, necessitating a careful re-evaluation of your budgeting strategy. It’s important to revisit and refine your budget periodically, taking into account these life changes.

Ultimately, the flexibility of the 50/30/20 rule is one of its greatest strengths. It serves as a framework, allowing for personalized adjustments based on individual circumstances and financial goals. The key is to be mindful of your spending and savings habits, regularly review your budget, and adjust the ratio as needed to maintain financial health and stability.

{kind=link}